According to American Economist, Burton Malkiel, “The surest way to find an actively managed fund that will have top-quartile returns is to look for a fund that has bottom-quartile expenses.”

Malkiel, author of A Random Walk Down Wall Street and chief investment officer of Wealthfront, is known for his strong sentiments against paying for investment fees. While his advice may be nothing new, his research shows active fund managers rarely outperform benchmark indexes and charge higher fees than low-cost index funds. The combination of underperformance and higher fees erodes returns over time.

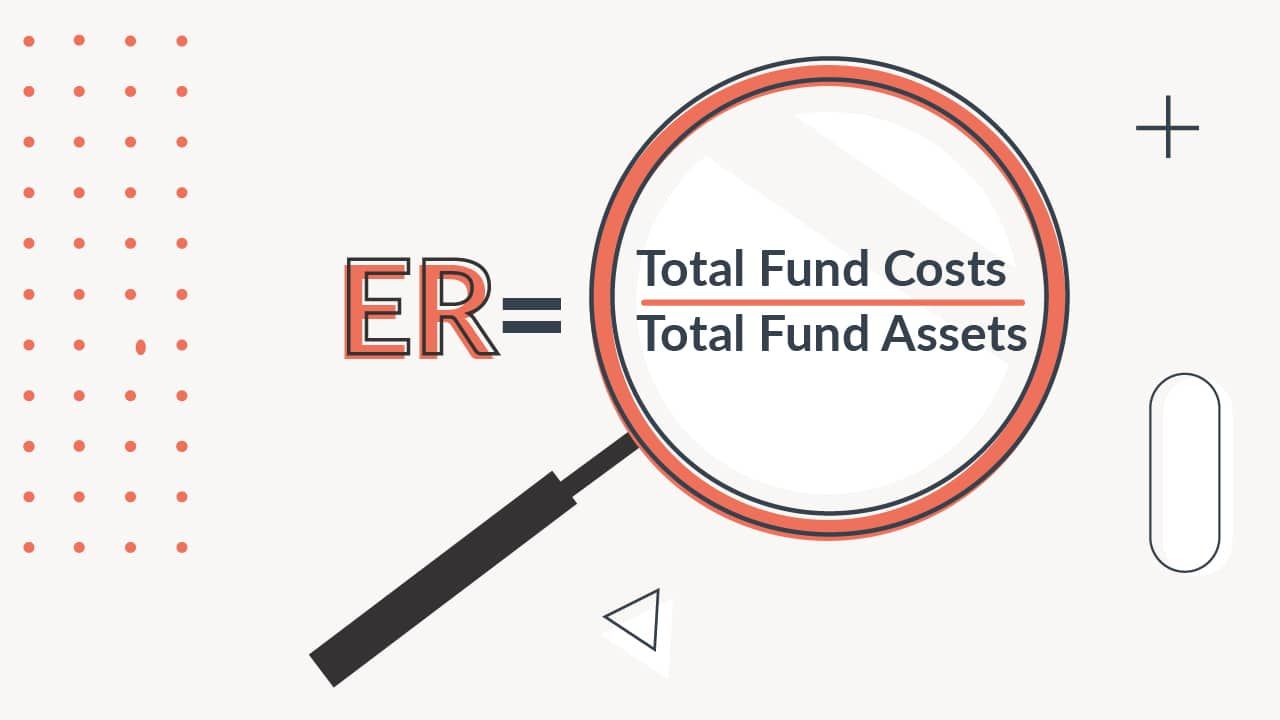

Malkiel is especially focused on the expense ratio, which is the cost of overhead and administrative fees, for owning mutual funds or exchange-traded funds (ETFs). Since a fund’s expenses are paid out of the fund’s assets, every dollar spent on expenses means that returns are reduced by a dollar.

If you’re investing in mutual funds or ETFs, it's critical to understand what an expense ratio is, and how much you’re paying for it.

Mutual Funds vs. ETFs: Understand The difference

Fees, types of investments available, dividend payouts, and availability based on account type all come into play when choosing between mutual funds and ETFs. Read more and find out what the differences are.

Expense Ratio Costs

The expense ratio is expressed as a ratio of the fund’s costs relative to the assets inside the fund. Expense ratios can range from 0% to 2.5% or more.

Typically, broad-based index funds have very low expense ratios. By contrast, actively managed funds tend to have higher expense ratios.

Why Expense Ratios Matter In Investing

Expense ratios matter in investing because fees eat into returns. A fund’s expenses are paid out from the assets. The costs associated with running the fund may erode the fund’s performance over time - the higher the expenses, the lower the return. Plus, expenses on a fund need to be paid whether the fund is up for the year or down.

An expense ratio serves as a drag on a fund’s overall performance. If two funds have identical asset allocations, the fund with the lower expense ratio will yield a higher return. Since so many funds have similar investment strategies, it makes sense to choose a fund with a lower expense ratio rather than one with a higher fee.

S&P500 Example

For example, say you want to invest in the S&P500. This is simply an index fund of the 500 stocks that make up the S&P500. The investments of all S&P500 index funds should be identical, so the biggest differentiator in performance will be the expense ratio - the fees you're being charged to own the same 500 stocks.

Here's two common S&P500 ETFs and their expense ratios:

ETF | Expense Ratio | 1-Year Return | 5-Year Return |

|---|---|---|---|

VOO | 0.03% | -2.51% | 13.88% |

SPY | 0.0945% | -2.52% | 13.82% |

As you can see, SPY has an expense ratio of 3x more than VOO. As a result, its performance is lower over time. And the higher the expenses, the worse performance will be for the same investments.

If you’re curious about the expense ratios in your investment portfolio, consider using Morningstar to analyze your portfolio’s total fee structure.

Should You Avoid Paying Expense Ratios?

In certain investment communities, avoiding fees and expense ratios have become a substitute for an investment strategy. Fidelity, which has long been a low-cost leader brokerage, even introduced four, zero-fee ETFs.

Avoiding unnecessary fees certainly means you keep more money in your investment account. However, it doesn’t mean an expense ratio is a “bad fee” either. Sometimes, paying a small expense ratio on your investment funds can make it easier for you to stick to your investing strategy.

Over-focusing on expense ratios may lead to some ill-conceived investing behaviors. For example, an investor may eschew investments in their workplace 401(k) plan because all the fund options carry modest expenses. Others may rack up capital gains by selling a fund every time they find a lower-cost option.

Investing Numbers That May Matter More Than Expense Ratios

While slaying the fee dragon may feel good, it’s not the most important factor in wealth building. An investment portfolio means your focus should be on growing on these numbers and building wealth more than expense ratios.

Your savings rate

Your savings rate is the amount you save (and invest) relative to the amount you earn. Your personal savings rate is one of the primary drivers behind your ability to achieve financial independence. It is especially important to focus on this number in your early investment years.

- If you’re earning $40,000 per year, and you manage to set aside $6,000, you have a 15% savings rate.

- An income of $100,000 with $6,000 in savings only constitutes a 6% savings rate.

Overall Investment Rate Of Return

Your overall investment rate of return is the total growth and dividends earned expressed as an annual percentage. As your wealth grows, your overall investment returns become increasingly important.

- If you have $25,000 saved, an 8% rate of return yields $2000 in growth.

- A 10% rate of return yields $2,500. The $500 difference is driven entirely by your rate of return. The difference, which is already pronounced with a $25,000 portfolio becomes even larger as you add more zeros to your portfolio.

Of course, you can’t directly control your investment rate of return. Market returns fluctuate, and investment options that seemed reliable when you bought them may fail to produce a return.

One way to indirectly influence your rate of return is to focus on your asset allocation. Historically, stocks have produced the largest returns while other asset classes have had lower returns. However, a blend of different assets can produce more reliable returns which can boost your overall portfolio performance.

Your Tax Rate On Investments

Understanding the Federal Tax Code may seem like a daunting task for a typical DIY investor. But a basic grasp of taxes and investing can boost your investment returns. If you focus on tax efficient investing (like using retirement accounts, avoiding unnecessary capital gains taxes, and avoiding tax penalties), you can see higher returns than if you didn’t pay attention to these things.

Some investors, even those who prefer self-directed investments, can take advantage of tax provisions that reduce their tax burden.

Trading Fees

Low-cost brokerages make it possible to avoid trading fees on stocks, ETFs, and other common products.

However, many crypto brokerages still charge fees on every trade you make. Frequent traders may find that the fees they pay on crypto sites significantly erode their returns. If you’re dabbling in crypto trading, be sure to consider the fees when trading.

Final Takeaways

Minimizing your expense ratio can improve your portfolio’s overall performance and a tactic to boost return - especially when you're choosing between two funds that invest in the same thing.

However, it shouldn’t be the sole focus of your investment strategy. Before you get too caught up in the minutiae of your portfolio, make sure you have an overall investment strategy that supports your specific goals.

The Best Investment Strategy By Age [Ultimate Guide]

Here's how to craft the best investment strategy and why you should always think about your portfolio and all your money as a whole.

Hannah is a wife, mom, and described personal finance geek. She excels with spreadsheets (and puns)! She regularly explores in-depth financial topics and enjoys looking at the latest tools and trends with money.

Editor: Claire Tak